Mortgage insurance protects the lender from financial losses

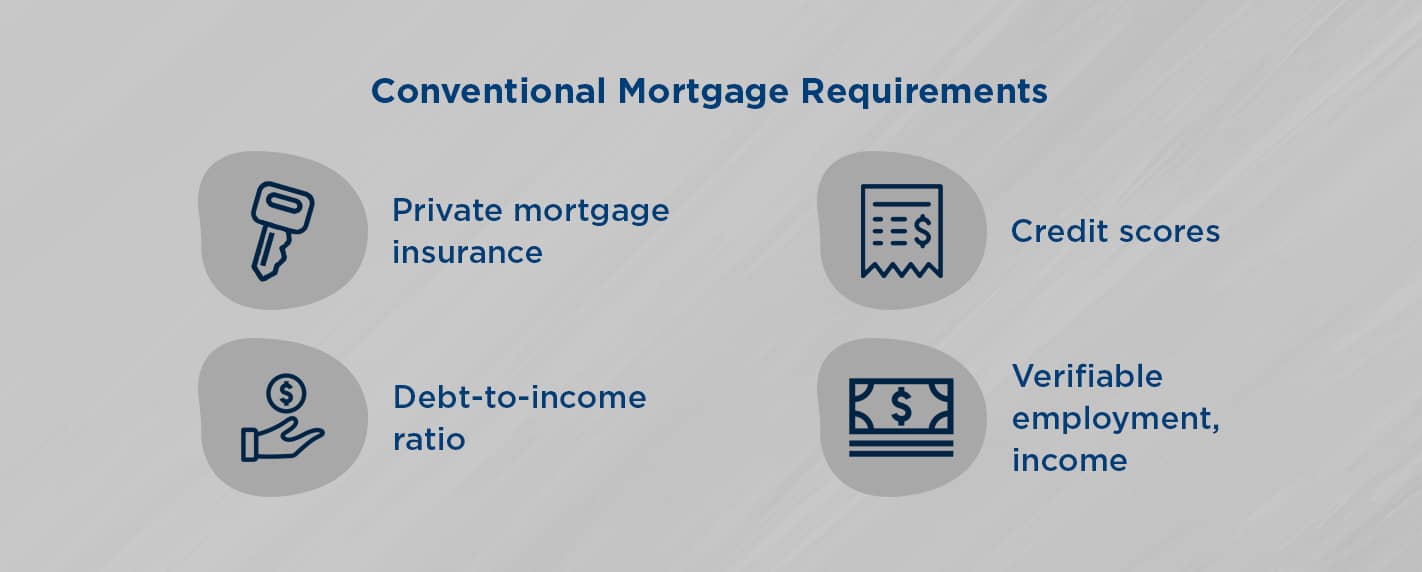

Mortgage insurance is designed to protect the lender against financial losses caused by nonpayment of a loan. It pays the legal fees and expenses incurred in closing a house. To offset the risk, the lender might charge a low interest on the loan.

This protection helps people with lower credit scores to purchase a home. You may also need it for certain government-backed loan programs. Mortgage insurance is essential for those who have lower credit scores and whose credit is not excellent. It helps the lender in the case of a default or foreclosure because the lender can recoup its losses.

It is required on 90% LTV fixed mortgages

Lenders have protection against financial loss if borrowers default. Mortgage insurance is called mortgage insurance. Both federal and private mortgage insurance laws require that borrowers purchase insurance on an annual and upfront basis. FHA mortgages require that all loans be insured, regardless of their amortization period and LTV ratio. In certain instances, mortgage insurance may not be necessary.

The loan-to-value ratio (LTV) is an important calculation in determining mortgage rates. It also determines the lender's riskiness of the loan. LTV determines the lender's risk. Avoid an underwater mortgage by looking at comparable homes in the area.

The borrower pays it each month.

The monthly payment of mortgage insurance is made by the borrower. This protects the lender in case the borrower defaults. The loan amount, length, and amount of down payment determine the amount of insurance premium. A small down payment could mean that a borrower would only need to pay $166 per monthly for mortgage insurance. As the borrower repays the loan, this amount will decrease each year.

The cost for mortgage insurance is 1.75%. It is possible to choose to pay it all at closing or to have it financed in part of your mortgage payment. It generally costs between $30-$70 per $100,000 borrowed. If the borrower builds up 20% equity in the property after a year, mortgage insurance coverage will end automatically. The cost of the insurance will rise if the borrower defaults on the mortgage payment.

FAQ

What is a Reverse Mortgage?

A reverse mortgage is a way to borrow money from your home without having to put any equity into the property. This reverse mortgage allows you to take out funds from your home's equity and still live there. There are two types to choose from: government-insured or conventional. A conventional reverse mortgage requires that you repay the entire amount borrowed, plus an origination fee. FHA insurance covers the repayment.

How can I find out if my house sells for a fair price?

It could be that your home has been priced incorrectly if you ask for a low asking price. If your asking price is significantly below the market value, there might not be enough interest. To learn more about current market conditions, you can download our free Home Value Report.

What are the pros and cons of a fixed-rate loan?

With a fixed-rate mortgage, you lock in the interest rate for the life of the loan. This guarantees that your interest rate will not rise. Fixed-rate loans have lower monthly payments, because they are locked in for a specific term.

How much does it cost for windows to be replaced?

Replacement windows can cost anywhere from $1,500 to $3,000. The total cost of replacing all your windows is dependent on the type, size, and brand of windows that you choose.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to become an agent in real estate

You must first take an introductory course to become a licensed real estate agent.

Next, you will need to pass a qualifying exam which tests your knowledge about the subject. This requires that you study for at most 2 hours per days over 3 months.

After passing the exam, you can take the final one. In order to become a real estate agent, your score must be at least 80%.

If you pass all these exams, then you are now qualified to start working as a real estate agent!