Cash out refinance enables you to take out a lump-sum loan in exchange for the remaining balance on your mortgage. The loan agreement you sign will be different from the original mortgage. It will contain a different interest, repayment term, loan amount, and repayment terms. This type of loan allows you to borrow for up to 30 year to repay the loan. You can choose from a fixed or adjustable rate. This loan can be used for many purposes, including home improvements and tax savings.

Cash-out refinances pay off your existing mortgage

A cash-out refinance can be a great way to pay off your mortgage and purchase a new home. These types of refinances require a lower down payment and are ideal for home improvements. However, you should be aware of the risks of cash-out refinances and consult with a financial planner or accountant before applying for one. A cash-out refinance will also require an appraisal of your existing property. This appraisal is required before you can apply for a cash loan.

Compared to other ways of leveraging home equity, cash-out refinances require only a single monthly payment. These refinances allow you to use the money for whatever purpose you choose, such as debt consolidation or a child's college education. The best part about cash-out refinances is that they usually have lower interest rates than other types of loans. A cash-out refinance can help you pay off your high-interest credit cards, which could save you thousands of dollars in interest payments. Also, it can increase your credit score by paying off all of your credit card debts.

Second mortgages are home equity loans

Home equity loans are a type second mortgage that use the equity remaining in a homeowner’s home as collateral. It is a great option to consolidate your debts into one low-interest payment and receive a lower rate of mortgage. These loans usually have fixed interest rates and monthly payments, so there are no unexpected surprises. Another benefit of home equity loans are that the funds are generally given in a lump sum so the borrower is able to budget accordingly.

You can get home equity loans quickly and enjoy many benefits. They are a great way to obtain cash quickly and are often tax-deductible. The process is simple, though you will need credit checks and to order an appraisal for your home.

They have higher interest rates than cash-out refinances

A cash-out refinance can be a beneficial option if you need a large sum of money quickly. This can however be more expensive than a mortgage or home equity loan. Moreover, cash-out refinances require a high credit score and have higher underwriting standards.

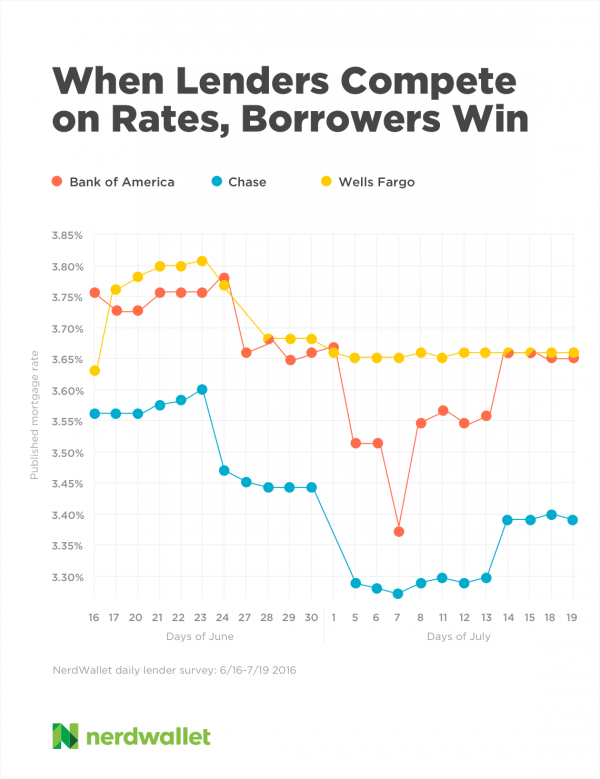

Refinance your mortgage with cash-out. In return, you'll only pay one monthly fee instead of many. Variable interest rates can apply to home equity loans, and these may rise as the loan term continues. Therefore, it is important to shop around for the best rates available and terms that are right for you.

They enable you to take money from your house prior to you sell it.

Home equity loans, also known as cash out refinance, are home loans that allow you to take money from your home before it is sold. You can use this money to pay down debt or to cover large-scale expenses. Some borrowers use the money to fund education, emergency savings, or other large expenses. These loans have some drawbacks.

A cash out refinance involves refinancing your mortgage to a larger one. You then receive a check at closing for the difference between the old and new mortgage balance. The money can be used for any purpose you choose. According to a recent Freddie Mac study, the most popular use of a cash out refinance is to pay off debt. The cash can also be used for home improvement or school costs.

FAQ

What is the maximum number of times I can refinance my mortgage?

This depends on whether you are refinancing with another lender or using a mortgage broker. You can typically refinance once every five year in either case.

Is it possible to get a second mortgage?

However, it is advisable to seek professional advice before deciding whether to get one. A second mortgage is often used to consolidate existing loans or to finance home improvement projects.

What should I look out for in a mortgage broker

Mortgage brokers help people who may not be eligible for traditional mortgages. They compare deals from different lenders in order to find the best deal for their clients. This service is offered by some brokers at a charge. Others offer free services.

How do I calculate my interest rate?

Market conditions impact the rates of interest. The average interest rate for the past week was 4.39%. Add the number of years that you plan to finance to get your interest rates. If you finance $200,000 for 20 years at 5% annually, your interest rate would be 0.05 x 20 1.1%. This equals ten basis point.

Can I buy my house without a down payment

Yes! There are many programs that can help people who don’t have a lot of money to purchase a property. These programs include FHA loans, VA loans. USDA loans and conventional mortgages. Check out our website for additional information.

What flood insurance do I need?

Flood Insurance covers flood damage. Flood insurance helps protect your belongings and your mortgage payments. Learn more about flood coverage here.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How to Manage a Rental Property

While renting your home can make you extra money, there are many things that you should think about before making the decision. We'll show you what to consider when deciding whether to rent your home and give you tips on managing a rental property.

Here are the basics to help you start thinking about renting out a home.

-

What factors should I first consider? You need to assess your finances before renting out your home. If you have debts, such as credit card bills or mortgage payments, you may not be able to afford to pay someone else to live in your home while you're away. You should also check your budget - if you don't have enough money to cover your monthly expenses (rent, utilities, insurance, etc. It might not be worth the effort.

-

How much will it cost to rent my house? It is possible to charge a higher price for renting your house if you consider many factors. These factors include your location, the size of your home, its condition, and the season. Keep in mind that prices will vary depending upon where you live. So don't expect to find the same price everywhere. Rightmove estimates that the market average for renting a 1-bedroom flat in London costs around PS1,400 per monthly. This means that your home would be worth around PS2,800 per annum if it was rented out completely. While this isn't bad, if only you wanted to rent out a small portion of your house, you could make much more.

-

Is it worth it. Doing something new always comes with risks, but if it brings in extra income, why wouldn't you try it? It is important to understand your rights and responsibilities before signing anything. Renting your home won't just mean spending more time away from your family; you'll also need to keep up with maintenance costs, pay for repairs and keep the place clean. Before you sign up, make sure to thoroughly consider all of these points.

-

What are the benefits? It's clear that renting out your home is expensive. But, you want to look at the potential benefits. There are plenty of reasons to rent out your home: you could use the money to pay off debt, invest in a holiday, save for a rainy day, or simply enjoy having a break from your everyday life. It's more fun than working every day, regardless of what you choose. If you plan ahead, rent could be your full-time job.

-

How do you find tenants? Once you decide that you want to rent out your property, it is important to properly market it. Make sure to list your property online via websites such as Rightmove. After potential tenants have contacted you, arrange an interview. This will allow you to assess their suitability, and make sure they are financially sound enough to move into your house.

-

How can I make sure I'm covered? If you fear that your home will be left empty, you need to ensure your home is protected against theft, damage, or fire. You will need to insure the home through your landlord, or directly with an insurer. Your landlord may require that you add them to your additional insured. This will cover any damage to your home while you are not there. This doesn't apply to if you live abroad or if the landlord isn’t registered with UK insurances. In such cases you will need a registration with an international insurance.

-

It's easy to feel that you don't have the time or money to look for tenants. This is especially true if you work from home. Your property should be advertised with professionalism. Make sure you have a professional looking website. Also, make sure to post your ads online. You'll also need to prepare a thorough application form and provide references. While some people prefer to handle everything themselves, others hire agents who can take care of most of the legwork. Interviews will require you to be prepared for any questions.

-

What happens once I find my tenant If there is a lease, you will need to inform the tenant about any changes such as moving dates. Otherwise, you can negotiate the length of stay, deposit, and other details. Keep in mind that you will still be responsible for paying utilities and other costs once your tenancy ends.

-

How do I collect rent? You will need to verify that your tenant has actually paid the rent when it comes time to collect it. You will need to remind your tenant of their obligations if they don't pay. Before you send them a final invoice, you can deduct any outstanding rent payments. You can always call the police to help you locate your tenant if you have difficulty getting in touch with them. They will not usually evict someone unless they have a breached the contract. But, they can issue a warrant if necessary.

-

How do I avoid problems? It can be very lucrative to rent out your home, but it is important to protect yourself. Consider installing security cameras and smoke alarms. You should also check that your neighbors' permissions allow you to leave your property unlocked at night and that you have adequate insurance. You should never allow strangers into your home, no matter how they claim to be moving in.