It is possible to save money by getting a mortgage using a point system. This article will discuss the benefits and costs of purchasing points. Also, we'll discuss when to buy points. We will also cover the tax benefits, break-even point and other details. Homeowners will love to make points investments on their mortgage.

Tax benefits

A 1 point mortgage can be a mortgage expense that may be deductible for certain taxpayers. The mortgage expense usually has a tax benefit of $750,000. Points are payable upfront and are independent of any closing costs such credit check fees, title insurance, application fees, recording and attorneys fees. The IRS allows points to be deducted as mortgage interest. This lowers taxable income. It also results in a lower refund and tax bill. But, before a mortgage points can be deducted, there are some conditions.

Mortgage points can help you get maximum tax savings. You need to think about how long you plan on staying in your home. Paying a point is good if you plan on living in the home for less than seven years. A mortgage point may not be necessary if you intend to sell the house or refinance it in the near future.

Prices

Mortgage points can reduce your mortgage rate. They are beneficial to borrowers who plan on staying in their homes for a prolonged period. These programs are not appropriate for all homebuyers. If you are planning to stay in your house for a long period of time, you should only consider a mortgage-point program. It is important to consider your budget before making any final decisions.

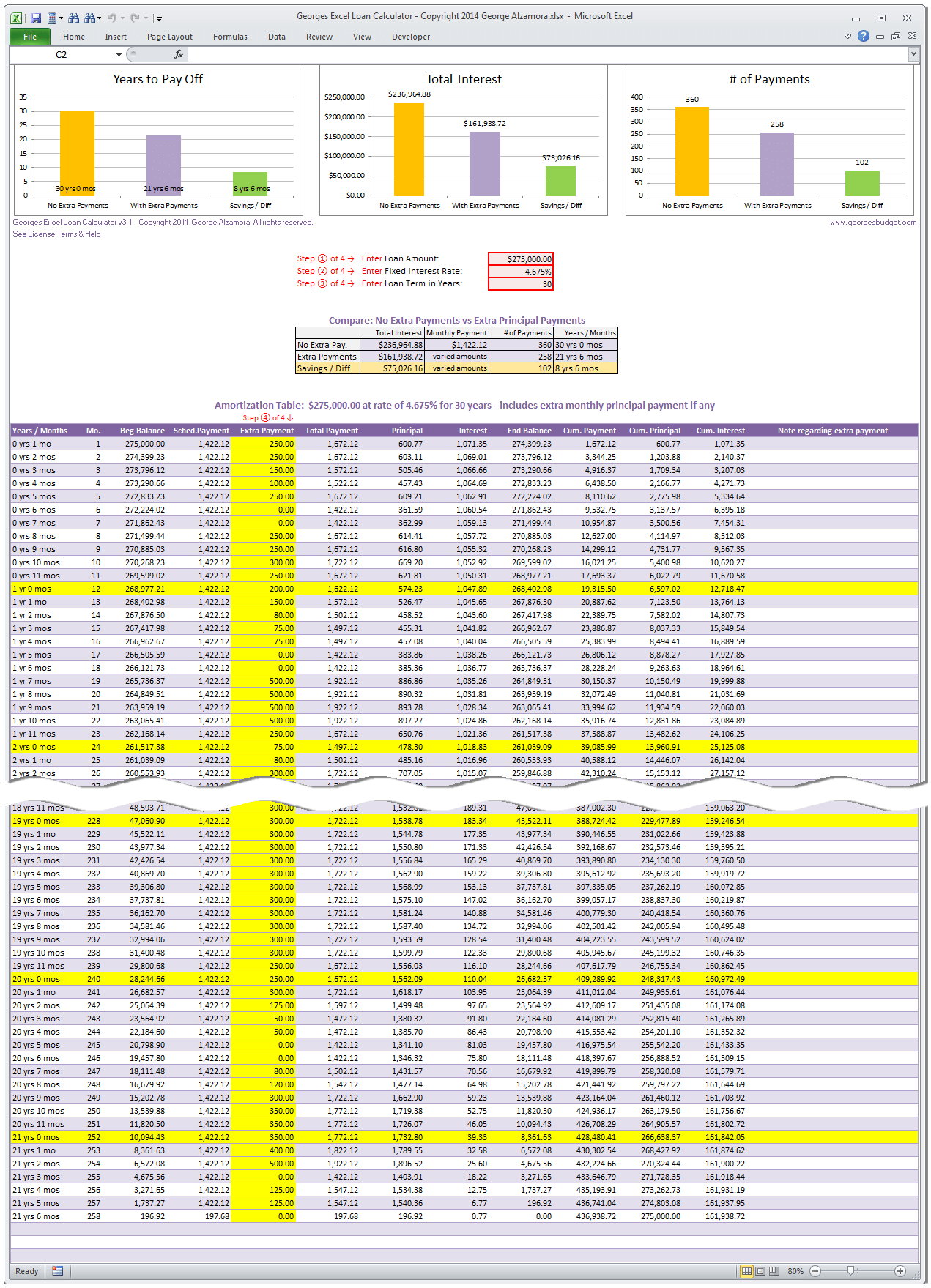

Before buying mortgage points, you should calculate how much you will save in the long run. There are many factors that will affect the amount of money that you can save each year, such as your location and job. The break-even period for your points on your mortgage should be calculated.

Break-even point

In order to determine whether or not paying one mortgage point is worth it, calculate your break even point. Your financial situation and housing plans will impact the amount of your break-even point. You should consider buying down your mortgage rate rather than paying points if you want to repay your loan faster. Consider how long you intend to be living in your home. It is not a smart investment to pay a point if your goal is to move in the next 10 years.

You can refinance your mortgage at a lower rate of interest, in addition to paying down the mortgage sooner. This will lower your monthly payments, and will save you money in the long run. The average break-even point for refinancing mortgages is 36 months.

Buying points

Buying points on a mortgage may help you get a lower interest rate, but this option may not be the best option for every home buyer. If you plan to live in your home for a while, it is worth considering purchasing points. Points purchase can lower your monthly loan payment and save you thousands in interest over the term of your loan.

Mortgage points are a special payment made at the closing of a mortgage that can lower your monthly payments and interest rate. This process is also known as "buying down the rate." The purchase of points can lower your mortgage payments and help you get closer to owning your house sooner.

Impairment of tax

One point can be deducted from your mortgage loan amount when you're approved. These mortgage points are listed on your settlement statement, or Box 6 on Form 1098. These points can be deducted over the life-of the loan, if you meet certain conditions. These criteria include the loan amount and whether the points are paid using your own funds.

To claim a deduction for a mortgage, you must use the money to buy your primary residence. If you rent, this deduction is not available to you.

FAQ

What are the key factors to consider when you invest in real estate?

You must first ensure you have enough funds to invest in property. You can borrow money from a bank or financial institution if you don't have enough money. Aside from making sure that you aren't in debt, it is also important to know that defaulting on a loan will result in you not being able to repay the amount you borrowed.

It is also important to know how much money you can afford each month for an investment property. This amount should include mortgage payments, taxes, insurance and maintenance costs.

Also, make sure that you have a safe area to invest in property. It would be a good idea to live somewhere else while looking for properties.

Should I use a mortgage broker?

A mortgage broker is a good choice if you're looking for a low rate. Brokers have relationships with many lenders and can negotiate for your benefit. Some brokers receive a commission from lenders. Before signing up for any broker, it is important to verify the fees.

How much money should I save before buying a house?

It all depends on how long your plan to stay there. Start saving now if your goal is to remain there for at least five more years. But, if your goal is to move within the next two-years, you don’t have to be too concerned.

What are the downsides to a fixed-rate loan?

Fixed-rate loans are more expensive than adjustable-rate mortgages because they have higher initial costs. If you decide to sell your house before the term ends, the difference between the sale price of your home and the outstanding balance could result in a significant loss.

How can I get rid Termites & Other Pests?

Termites and other pests will eat away at your home over time. They can cause severe damage to wooden structures, such as decks and furniture. A professional pest control company should be hired to inspect your house regularly to prevent this.

How long does it take to sell my home?

It depends on many factors, such as the state of your home, how many similar homes are being sold, how much demand there is for your particular area, local housing market conditions and more. It can take anywhere from 7 to 90 days, depending on the factors.

Statistics

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How to buy a mobile home

Mobile homes are houses constructed on wheels and towed behind a vehicle. Mobile homes are popular since World War II. They were originally used by soldiers who lost their homes during wartime. People who want to live outside of the city are now using mobile homes. These houses come in many sizes and styles. Some houses can be small and others large enough for multiple families. Some are made for pets only!

There are two main types of mobile homes. The first is built in factories by workers who assemble them piece-by-piece. This takes place before the customer is delivered. You could also make your own mobile home. You'll need to decide what size you want and whether it should include electricity, plumbing, or a kitchen stove. Next, ensure you have all necessary materials to build the house. Final, you'll need permits to construct your new home.

If you plan to purchase a mobile home, there are three things you should keep in mind. First, you may want to choose a model that has a higher floor space because you won't always have access to a garage. A model with more living space might be a better choice if you intend to move into your new home right away. The trailer's condition is another important consideration. Problems later could arise if any part of your frame is damaged.

Before buying a mobile home, you should know how much you can spend. It is important to compare the prices of different models and manufacturers. Also, consider the condition the trailers. While many dealers offer financing options for their customers, the interest rates charged by lenders can vary widely depending on which lender they are.

You can also rent a mobile home instead of purchasing one. Renting allows you the opportunity to test drive a model before making a purchase. Renting is not cheap. Renters typically pay $300 per month.