A HELOC is a loan that allows you to borrow the maximum amount for your home. This loan allows the borrower to borrow the most amount possible for a limited time. Your home's equity will provide security for the money you borrow. You should be aware of what your lender expects before you apply to a HELOC. If your equity is not sufficient, you may need to have an appraisal.

A heloc

It is important to understand what you can expect from a HELOC application. HELOCs are loans that use the equity in your house as collateral. Lenders will normally lend you as much money as possible within a specified timeframe. It is important to understand what this type of loan involves and how to get the best deal. Many people are unsure if they should get an appraisal for a HELOC.

A HELOC appraisal will show the lender what your home is worth. The lender will need to know what equity you have and how much debt you have against your home. For any home loan process, it is necessary to have a home valuation. It will also protect both the borrower and the lender.

How to get a second loan

Although a second mortgage can be a great way of borrowing against your home equity, there are many things you should consider before applying. Your existing equity is essential to the lending process, and the lender will require an appraisal of it. This document will provide information on how much equity you own and how much the loan is likely to be.

The lender will also want to look at your credit score. The lender will look at your credit score as a key factor in your second loan approval. Other than the appraisal, additional fees may apply such as survey fees or attorney fees. Fees for disclosure reports on flood and natural hazards and other fees may also be payable. The cost of title insurance is another common expense.

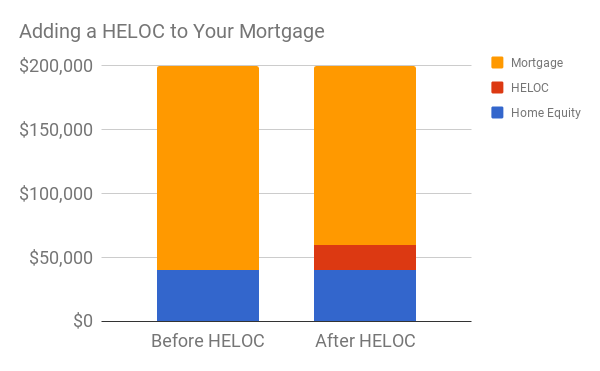

Appraisal

A home equity credit, or HELOC is a loan you can get that is based on the equity of your home. This type of loan allows you to borrow the maximum amount within a specified period of time. For you to be eligible, your credit score must be at least 620 and you must have a low debt/income ratio. A home appraisal is important because it helps the lender know how much you owe against your home. But the appraisal is not absolutely necessary. An appraisal is not necessary. You can use financial intuition to estimate how much equity your have.

The appraiser will inspect your home from the outside and collect information about its features. They will also inspect your home and compare it to similar properties in the same area. They will also evaluate any improvements that have been made to the exterior of your home.

Combining a reverse-mortgage with a heloc to obtain a heloc

Certain qualifications are required to obtain a reverse-mortgage. A thorough appraisal of the property is required. If the property is worth less than the appraisal, you might want to choose the line of credit option instead. However, regular monthly payments are required for a credit line. This can lead to credit problems or foreclosure. In contrast, a reverse mortgage does not require monthly payments, but it is less expensive to establish. You will need to live in your property and pay all taxes and insurance on the due date.

Your ability to repay the reverse mortgage you apply for is one of the most important factors. HELOCs, as well as reverse mortgages, use the ability repay method. This determines a borrower’s ratio of debt to income. For those with a fixed income, the former is more accessible.

FAQ

How do I eliminate termites and other pests?

Termites and many other pests can cause serious damage to your home. They can cause severe damage to wooden structures, such as decks and furniture. This can be prevented by having a professional pest controller inspect your home.

What are the benefits of a fixed-rate mortgage?

Fixed-rate mortgages lock you in to the same interest rate for the entire term of your loan. This means that you won't have to worry about rising rates. Fixed-rate loans also come with lower payments because they're locked in for a set term.

What should I consider when investing my money in real estate

It is important to ensure that you have enough money in order to invest your money in real estate. You can borrow money from a bank or financial institution if you don't have enough money. It is important to avoid getting into debt as you may not be able pay the loan back if you default.

You must also be clear about how much you have to spend on your investment property each monthly. This amount must include all expenses associated with owning the property such as mortgage payments, insurance, maintenance, and taxes.

Finally, ensure the safety of your area before you buy an investment property. It would be best if you lived elsewhere while looking at properties.

What can I do to fix my roof?

Roofs may leak from improper maintenance, age, and weather. Roofers can assist with minor repairs or replacements. Contact us for further information.

Can I get another mortgage?

Yes. But it's wise to talk to a professional before making a decision about whether or not you want one. A second mortgage is often used to consolidate existing loans or to finance home improvement projects.

What is the average time it takes to get a mortgage approval?

It depends on many factors like credit score, income, type of loan, etc. Generally speaking, it takes around 30 days to get a mortgage approved.

Statistics

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

External Links

How To

How to find houses to rent

People who are looking to move to new areas will find it difficult to find houses to rent. But finding the right house can take some time. Many factors affect your decision-making process when choosing a home. These factors include price, location, size, number, amenities, and so forth.

It is important to start searching for properties early in order to get the best deal. Also, ask your friends, family, landlords, real-estate agents, and property mangers for recommendations. This will ensure that you have many options.