A home equity mortgage is a type second mortgage that allows the borrower to access your equity. You can use it for many purposes. It is also tax-deductible. This is a great way for you to cover unexpected expenses. A home equity loan is a great way to reach your financial goals, whether you are looking for money to start a business or expand your family.

A form of second mortgage, home equity loans can be used to finance your home.

Home equity loans can be a great way to consolidate debts. Before you take out a second loan, determine the monthly payment amount. Make sure that the loan will be lower in interest than your other obligations. You should also ensure that the loan term is longer than any other debts.

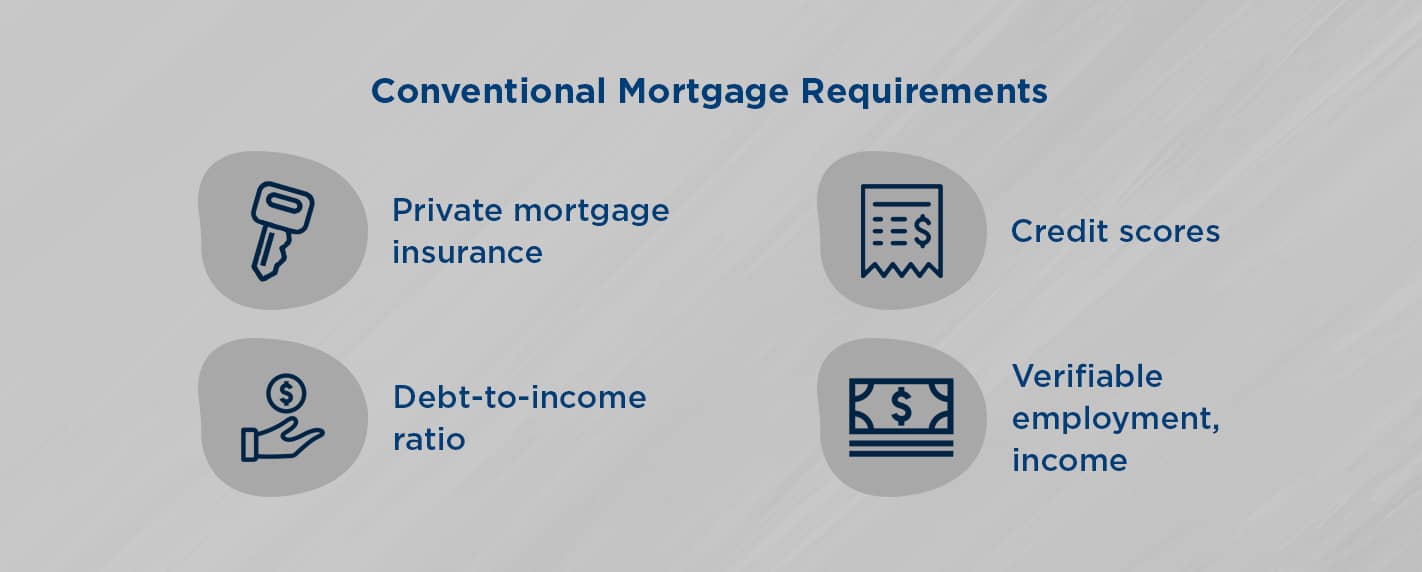

A review and application process is required for home equity loans. Lenders consider many factors, including your income and credit history. These factors, as well your credit score, income, debt-to–income ratio, and credit history, will all affect how much money you can borrow. You shouldn't borrow more than 80 percent of the value your home.

They are protected by your equity in your home

A home equity loan is a secured loan that is secured by the equity in your home. You may be eligible for up to 80 percent of the home's total value. Whether you can qualify will depend on your employment history, credit score and income. The higher your credit score, the lower your risk of default and the lower your interest rate.

Home equity refers to the difference between your home's current market value and your outstanding mortgage balance. Home equity loans let you access the equity in your home without needing to repay your current mortgage balance. These loans usually have lower interest rates that traditional loans. However, they must be paid back, and lenders may foreclose on your home if you don't meet the agreed-upon terms.

These items are tax-deductible

Home equity loans allow you to deduct interest from your taxes. This interest can be claimed using Schedule A, an IRS tax form. You can either claim the interest yourself or with the assistance of a tax professional. Keep all receipts for home improvements and home equity loan expenses. Also keep receipts of materials, labor, permits and permits you use to make improvements.

Many benefits make home equity loans a great option for borrowers. They offer low interest rates and can be used as a way to consolidate large debts. They are also able to provide funding for large purchases or education. You may be able to qualify for a competitive rate on your home equity loan.

FAQ

What is a reverse mortgage?

A reverse mortgage lets you borrow money directly from your home. This reverse mortgage allows you to take out funds from your home's equity and still live there. There are two types: government-insured and conventional. If you take out a conventional reverse mortgage, the principal amount borrowed must be repaid along with an origination cost. If you choose FHA insurance, the repayment is covered by the federal government.

Is it possible fast to sell your house?

It may be possible to quickly sell your house if you are moving out of your current home in the next few months. There are some things to remember before you do this. First, you will need to find a buyer. Second, you will need to negotiate a deal. Second, prepare your property for sale. Third, you must advertise your property. You must also accept any offers that are made to you.

Should I rent or own a condo?

Renting may be a better option if you only plan to stay in your condo a few months. Renting saves you money on maintenance fees and other monthly costs. A condo purchase gives you full ownership of the unit. The space can be used as you wish.

How can I eliminate termites & other insects?

Termites and many other pests can cause serious damage to your home. They can cause serious damage and destruction to wood structures, like furniture or decks. It is important to have your home inspected by a professional pest control firm to prevent this.

How long does it take for my house to be sold?

It depends on many different factors, including the condition of your home, the number of similar homes currently listed for sale, the overall demand for homes in your area, the local housing market conditions, etc. It may take up to 7 days, 90 days or more depending upon these factors.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to be a real-estate broker

Attending an introductory course is the first step to becoming a real-estate agent.

The next thing you need to do is pass a qualifying exam that tests your knowledge of the subject matter. This means that you will need to study at least 2 hours per week for 3 months.

Once this is complete, you are ready to take the final exam. You must score at least 80% in order to qualify as a real estate agent.

These exams are passed and you can now work as an agent in real estate.