You should shop around for the best rate for you if you are looking to get a mortgage. Shopping around could save you thousands of dollars over your loan's life. Some studies show that borrowers who shop around for the best mortgage rate save an average of $1,500. This is a significant savings, especially if you get five quotes from different lenders. It is important to get the best rate and to choose a lender that offers you the terms you desire. Many lenders are online and will preapprove you within minutes.

Factors that impact mortgage rates

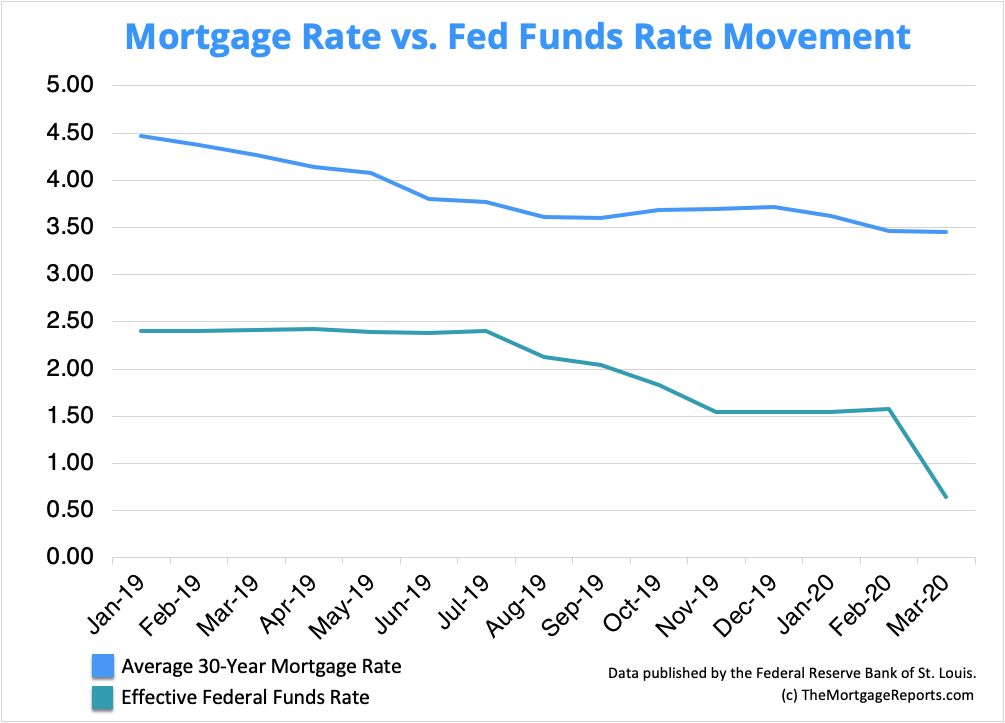

There are many factors that affect mortgage rates, including the borrower's credit history and financial health. The type of mortgage and the length of the repayment period also influence rates. The Federal Reserve also affects mortgage rates by changing short-term interest rates, which govern how banks lend money. However, the economy and the state of the economy are also factors that affect mortgage rates.

The Federal Reserve is the central authority on mortgage rates. It uses its influence to manage inflation. To keep interest rates low, the Fed can purchase securities through the U.S. Treasury when there is an economic crisis. This reduces bank lending and therefore lowers the price for mortgage loans.

Another factor that can affect mortgage rates is the stock exchange. Stock prices indicate investor confidence in the economy. Mortgage rates will rise if stock prices rise. In the opposite direction, if stock prices fall, mortgage interest rates will rise.

How to compare rates on mortgages

It is important that you compare rates and lenders when you're looking for a mortgage. You can use this benchmark to compare lenders. The average interest rate on a 30-year fixed-rate mortgage was 5.36 percent. But, mortgage rates can differ greatly from lender-to-lender.

After the collapse of the housing bubble in 2006, the market for mortgages began to recover. Prices are rising and negative equity debts have fallen from an all-time high of 25%. The government is also trying to regulate the mortgage industry in order to make it safer for investors. A recent report by The Economist, a well-respected financial analyst firm, stated that the mortgage market is still dangerously under-capitalized.

Before you can compare mortgage rates, check that your eligibility is verified. This can be done at your bank, broker or online. It is also helpful to use the average nationwide mortgage rate as a benchmark. YCharts and MarketWatch are three of the most well-known mortgage rate comparison websites. These comparison sites will help you easily and efficiently compare mortgage rate.

How to get a low rate mortgage

If you are thinking about purchasing a home, the best way to get the lowest mortgage rate possible is to shop around for a lender. You can search online for reviews and testimonials, or talk to friends who have recently bought a home. Next, compare rates and submit loan applications to multiple lenders. The best mortgage lender will depend on your financial situation.

While mortgage rates change every year there are some things you can do that will keep your interest rates low. A good credit rating and a large downpayment are two ways to achieve this. You can also try different mortgage calculators to lower your mortgage rate. A mortgage calculator can help you determine what the different rates are going to cost you monthly.

Since the start of the year, mortgage rates are on the rise. A good way to find a low mortgage rate is to work on your credit rating before you apply. Depending on the type of loan you select, this can help you save thousands of dollars. Negotiating with your lender is a good idea to obtain the lowest possible rate.

FAQ

Should I rent or buy a condominium?

If you plan to stay in your condo for only a short period of time, renting might be a good option. Renting can help you avoid monthly maintenance fees. A condo purchase gives you full ownership of the unit. You are free to make use of the space as you wish.

Can I get a second mortgage?

Yes. However, it's best to speak with a professional before you decide whether to apply for one. A second mortgage is often used to consolidate existing loans or to finance home improvement projects.

What are the benefits of a fixed-rate mortgage?

With a fixed-rate mortgage, you lock in the interest rate for the life of the loan. This will ensure that there are no rising interest rates. Fixed-rate loans come with lower payments as they are locked in for a specified term.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to Find an Apartment

Finding an apartment is the first step when moving into a new city. This involves planning and research. It includes finding the right neighborhood, researching neighborhoods, reading reviews, and making phone calls. This can be done in many ways, but some are more straightforward than others. Before renting an apartment, you should consider the following steps.

-

Online and offline data are both required for researching neighborhoods. Websites such as Yelp. Zillow. Trulia.com and Realtor.com are some examples of online resources. Offline sources include local newspapers, real estate agents, landlords, friends, neighbors, and social media.

-

Review the area where you would like to live. Yelp, TripAdvisor and Amazon provide detailed reviews of houses and apartments. You may also read local newspaper articles and check out your local library.

-

For more information, make phone calls and speak with people who have lived in the area. Ask them what they liked and didn't like about the place. Ask for their recommendations for places to live.

-

Take into account the rent prices in areas you are interested in. Consider renting somewhere that is less expensive if food is your main concern. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Find out more information about the apartment building you want to live in. How big is the apartment complex? What is the cost of it? Is it pet-friendly What amenities are there? Are you able to park in the vicinity? Do you have any special rules applicable to tenants?