If you have a low down payment or less than 80% LTV ratio on your mortgage, you may be wondering how to avoid PMI. There are several ways to cancel this type or insurance. These are the most popular ways to cancel this type of insurance. While a second mortgage may reduce your monthly payments but it will require you to incur additional closing costs.

Can I cancel my PMI if I pay less than 20%?

PMI is a government program homeowners must enroll in until they have attained 20% equity in their homes. It is expensive but it can lower interest rates. This is especially important if you have low down payment. They could be subject to higher interest rates.

It is not always possible to eliminate PMI. It is sometimes necessary for people who can't pay 20% of their purchase price. This program acts as a safety net and prevents lenders from financial loss.

Some lenders provide loans without PMI. FHA and VA loans require no PMI. Private lenders may also offer conventional loans without PMI with small down payments. Private lenders charge higher rates to offset the risk. After you have reached 20 percent equity, you may request an automatic termination/final cancellation of PMI.

Can I cancel PMI when I have less than 78% of my LTV?

The law that governs private mortgage insurance cancelation sets certain criteria that must be met in order for the policy to be cancelled. These criteria include owner's equity, time from mortgage origination and percentage of property value less than 78% LTV. In general, homeowners have two years from the date of the mortgage's origination to request cancellation. However, if an owner exceeds this threshold prior, the mortgage provider may deny the cancellation request.

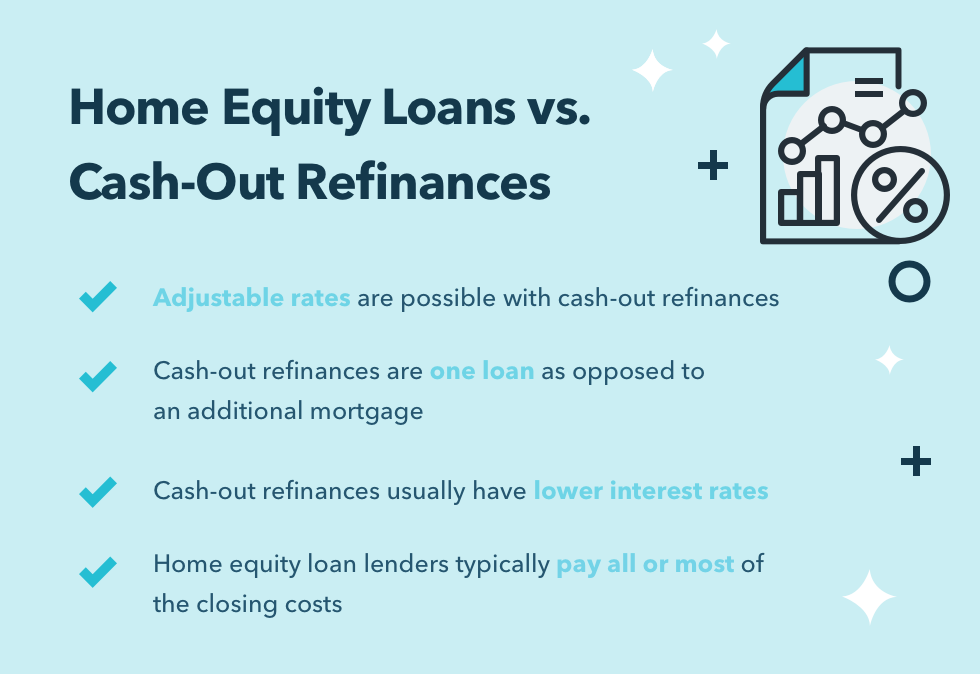

PMI is an add-on fee to your mortgage that is often unnecessary. PMI can be removed if the LTV ratio reaches 78%, and you have completed your first 36 payments. This is not always possible so you might consider making additional payments to eliminate PMI sooner. Refinancing your mortgage can make it less expensive if you don’t want to take out monthly mortgage insurance.

Can I cancel PMI if my credit score is higher

To cancel PMI, you must notify the lender in writing. In addition to being current on your payments, you will need to have a strong payment history. To determine the home's value, your lender might also request an appraisal. PMI can be canceled if you prove that there is 20% equity in your home.

A higher credit score can usually help you cancel your PMI faster. This is because lenders have different cancellation dates for high-risk loans. Sometimes, having a strong payment history can allow you to cancel your loan as soon as the LTV ratio is 80%.

A VA special program is available to veterans. You can cancel PMI and refinance your home with this program. It will only cost you a small upfront funding fee.

FAQ

Is it possible to quickly sell a house?

If you have plans to move quickly, it might be possible for your house to be sold quickly. There are some things to remember before you do this. First, you must find a buyer and make a contract. You must prepare your home for sale. Third, advertise your property. You must also accept any offers that are made to you.

Can I buy my house without a down payment

Yes! There are programs available that allow people who don't have large amounts of cash to purchase a home. These programs include FHA, VA loans or USDA loans as well conventional mortgages. Visit our website for more information.

Should I use an mortgage broker?

Consider a mortgage broker if you want to get a better rate. Brokers are able to work with multiple lenders and help you negotiate the best rate. Some brokers do take a commission from lenders. You should check out all the fees associated with a particular broker before signing up.

What are the benefits associated with a fixed mortgage rate?

Fixed-rate mortgages allow you to lock in the interest rate throughout the loan's term. This means that you won't have to worry about rising rates. Fixed-rate loans come with lower payments as they are locked in for a specified term.

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How to buy a mobile home

Mobile homes are houses constructed on wheels and towed behind a vehicle. Mobile homes are popular since World War II. They were originally used by soldiers who lost their homes during wartime. Mobile homes are still popular among those who wish to live in a rural area. Mobile homes come in many styles and sizes. Some houses have small footprints, while others can house multiple families. There are some even made just for pets.

There are two main types of mobile homes. The first is built in factories by workers who assemble them piece-by-piece. This is done before the product is delivered to the customer. Another option is to build your own mobile home yourself. You'll need to decide what size you want and whether it should include electricity, plumbing, or a kitchen stove. You'll also need to make sure that you have enough materials to construct your house. Finally, you'll need to get permits to build your new home.

If you plan to purchase a mobile home, there are three things you should keep in mind. A larger model with more floor space is better for those who don't have garage access. You might also consider a larger living space if your intention is to move right away. Third, you'll probably want to check the condition of the trailer itself. It could lead to problems in the future if any of the frames is damaged.

You should determine how much money you are willing to spend before you buy a mobile home. It's important to compare prices among various manufacturers and models. Also, look at the condition of the trailers themselves. While many dealers offer financing options for their customers, the interest rates charged by lenders can vary widely depending on which lender they are.

You can also rent a mobile home instead of purchasing one. You can test drive a particular model by renting it instead of buying one. Renting is not cheap. Renters usually pay about $300 per month.