You should be familiar with the basics of a mortgage before you apply. This includes the Interest rate, down payment, and Lender's assessment of your information. It is important to choose the right mortgage for your home purchase. It can make such a difference in your life as well as your finances.

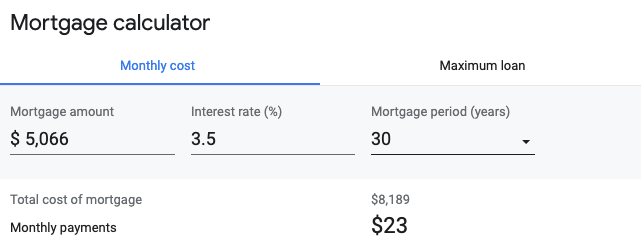

Rate of interest

The interest rate on a mortgage is a percentage of the total loan amount. The amount paid is in addition to the agreed loan payments. To be able make monthly payments, it is essential to select the best mortgage interest rate. Mortgage interest rates can increase as well as decrease, so it is important to keep a close eye on them.

Other costs related to the mortgage, such loan origination fees and discounts points, are not included in an interest rate. The closing costs and mortgage insurance are also included. The APR provides borrowers with a clear view of the total cost for borrowing.

Deposit payment

The down payment on a loan is a percentage of the property's total worth that the borrower will pay upfront. It usually ranges from ten to fifty percent. The interest rate that will be charged to a mortgage borrower will depend on the amount of their down payment. The interest rates will be lower for those who have made a larger down payment. A large downpayment lowers the risk for banks when they lend mortgages.

Although there is no set amount of down payment that you must make, there are certain factors you should take into consideration when making your down payments. Low down payments are risky. It's best to aim for at most fifty percent. Borrowers who are able to put up at least fifty percent to sixty percent of the purchase cost will be more likely to get money from a bank. A bank may refuse to lend money to you if you have a small down payment or if you don't have enough savings.

Lender's assessment of your information

A mortgage lender examines many factors to determine if your risk level. Your credit history and debt applications are just two examples of what they will consider. They may contact your employer to verify these details. They will also examine your payment history and check to see if your payments have been paid on time. They will also examine any substantial assets you may have.

Lenders want proof that you will be able pay back the loan. Lenders may also consider your creditworthiness or ability to manage more debt. They use the five Cs of credit to determine creditworthiness: capacity, character, capital, collateral, conditions, and conditions.

Types of mortgages

There are many types of mortgages. The first is a conventional mortgage. A conventional mortgage can be used on most property types. These loans are usually easier to get because they are guaranteed by the government. These mortgages are often more attractive for first-time homebuyers and those with lower credit scores and higher debt to income ratios.

The adjustable rate mortgage (ARM), is the second type. If you like to make adjustments to your interest rates, adjustable rate mortgages are the best choice. A government-backed loan is another option, such as an FHA or VA mortgage, or USDA mortgage.

Refinancing options

If you want to refinance your mortgage, there are many options available to you. You should shop around to find the best deal. Consider the current interest rate before you make a decision to refinance. You can also consult an attorney to assist you in the process.

Refinancing allows homeowners to make the most of their equity. It can lower your monthly payment and help you achieve your financial goals. Many people refinance their mortgages to lower interest rates, shorter payment terms, or cash out their home equity.

FAQ

What is the cost of replacing windows?

Replacing windows costs between $1,500-$3,000 per window. The total cost of replacing all your windows is dependent on the type, size, and brand of windows that you choose.

How can I get rid Termites & Other Pests?

Over time, termites and other pests can take over your home. They can cause serious damage and destruction to wood structures, like furniture or decks. It is important to have your home inspected by a professional pest control firm to prevent this.

How much money will I get for my home?

It all depends on several factors, including the condition of your home as well as how long it has been listed on the market. According to Zillow.com, the average home selling price in the US is $203,000 This

What should you think about when investing in real property?

It is important to ensure that you have enough money in order to invest your money in real estate. You will need to borrow money from a bank if you don’t have enough cash. It is important to avoid getting into debt as you may not be able pay the loan back if you default.

Also, you need to be aware of how much you can invest in an investment property each month. This amount must be sufficient to cover all expenses, including mortgage payments and insurance.

Also, make sure that you have a safe area to invest in property. You would be better off if you moved to another area while looking at properties.

What should I look for when choosing a mortgage broker

A mortgage broker assists people who aren’t eligible for traditional mortgages. They shop around for the best deal and compare rates from various lenders. Some brokers charge a fee for this service. Some brokers offer services for free.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How do I find an apartment?

When you move to a city, finding an apartment is the first thing that you should do. Planning and research are necessary for this process. This involves researching neighborhoods, looking at reviews and calling people. You have many options. Some are more difficult than others. Before renting an apartment, it is important to consider the following.

-

Researching neighborhoods involves gathering data online and offline. Online resources include websites such as Yelp, Zillow, Trulia, Realtor.com, etc. Offline sources include local newspapers, real estate agents, landlords, friends, neighbors, and social media.

-

Review the area where you would like to live. Yelp, TripAdvisor and Amazon provide detailed reviews of houses and apartments. You might also be able to read local newspaper articles or visit your local library.

-

Make phone calls to get additional information about the area and talk to people who have lived there. Ask them what they loved and disliked about the area. Ask them if they have any recommendations on good places to live.

-

Be aware of the rent rates in the areas where you are most interested. If you think you'll spend most of your money on food, consider renting somewhere cheaper. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Find out more information about the apartment building you want to live in. Is it large? How much is it worth? Is the facility pet-friendly? What amenities does it have? Do you need parking, or can you park nearby? Are there any special rules for tenants?