A down payment calculator helps you calculate how much money you need to put down on a home. These tools require information such the property's price, location, type of loan and credit score. They will automatically calculate the down payment amount based on the information you enter. A down payment calculator can help you determine how much you should budget for your down payment.

Bankrate's mortgage calculator allows you to determine how much money it will take to put down a downpayment.

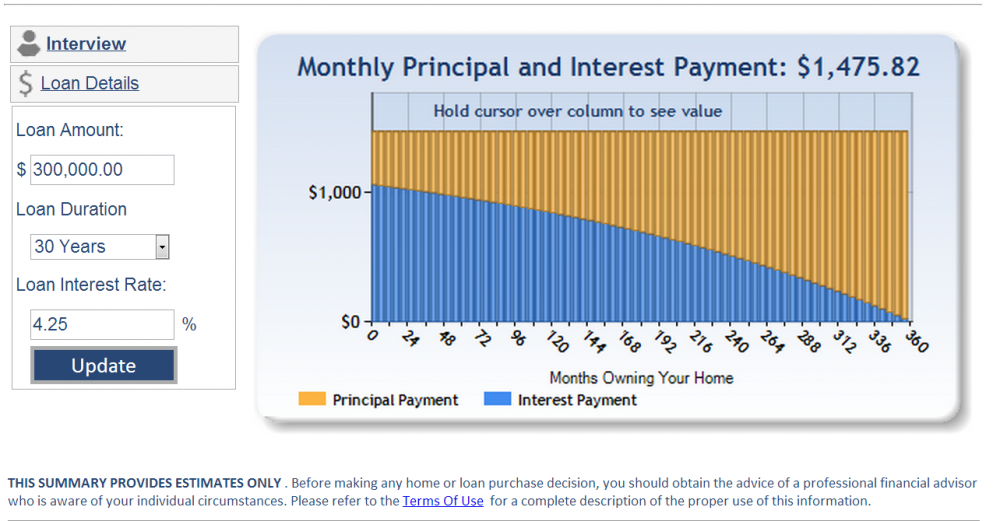

You can calculate how much down you will need with a mortgage calculator. A higher down payment will result in lower monthly payments and lower risks of getting mortgage insurance. A higher down payment will reduce interest costs and mortgage fees. The process can be made easier by using a mortgage calculator.

While most people concentrate on their down payment, it is important to factor in all the costs associated with owning a home. This can include insurance, property taxes, homeowners' association fees, and utilities. Using a mortgage calculator can help you figure out these costs and more.

20% down payment on a house you are interested in buying

There are many options when it comes to buying a house with a low down payment. Some lenders require as little as 3% down, and there are even programs that allow you to put zero down. It all depends upon your financial situation and goals. A 3% down payment is sufficient for first-time homebuyers. However, if you require more cash to close the deal, 20% may be required.

As this shows financial stability, homebuyers are more likely to be approved for mortgage loans. This can give you an edge in a competitive housing market. However, not everyone has the money to pay that amount. Others may prefer to save their cash for other purposes.

A smaller down payment? Save your money

A smaller down payment is a great way of building equity quicker. To start building equity faster, you must first figure out how much to save each monthly. A budgeting app can be used to calculate your monthly costs. You can also consult a financial advisor. When you have a budget for the month, you can start to look for areas you can trim. For your down payment, you will need to allocate a portion of your monthly income.

Switching jobs is a great way save for a small down payment. Although it will take a while for you to establish your budget, once that is done you'll be able set goals and prioritise your expenses you will have no trouble saving more for your downpayment. The average American spends 30 percent of their monthly income on other debts, such as credit cards, car loans, and educational loans. This means that most of us would have more money to save for a down payment.

Family and friends can help you.

You may be able to save more quickly for the down payment if you are in a tight time frame. Moving in with your parents or roommates can reduce your living expenses. You can then save money for your down payment. It is not easy to get a down payment loan. A loan will require you to pay more interest and fees.

A 20% down payment is required to avoid mortgage insurance

Many borrowers believe that the only way they can avoid private mortgage coverage is to pay a 20% downpayment. Due to the alarming rise in home values, this requirement has become increasingly difficult to meet. Additionally, it would be difficult to save enough money to buy a home first-time buyers. This could negatively affect the economy.

To avoid PMI even with a low down payment, borrowers may consider taking out a piggyback loan, a second loan that finances at least 10 percent of the home's value. The terms and interest rates of this second loan are different, but they can lower the monthly mortgage payments.

FAQ

What is a reverse loan?

A reverse mortgage is a way to borrow money from your home without having to put any equity into the property. It works by allowing you to draw down funds from your home equity while still living there. There are two types of reverse mortgages: the government-insured FHA and the conventional. With a conventional reverse mortgage, you must repay the amount borrowed plus an origination fee. FHA insurance will cover the repayment.

What amount of money can I get for my house?

The number of days your home has been on market and its condition can have an impact on how much it sells. The average selling price for a home in the US is $203,000, according to Zillow.com. This

What should I look out for in a mortgage broker

A mortgage broker is someone who helps people who are not eligible for traditional loans. They compare deals from different lenders in order to find the best deal for their clients. This service is offered by some brokers at a charge. Other brokers offer no-cost services.

Should I rent or purchase a condo?

Renting might be an option if your condo is only for a brief period. Renting saves you money on maintenance fees and other monthly costs. The condo you buy gives you the right to use the unit. You have the freedom to use the space however you like.

Do I need a mortgage broker?

If you are looking for a competitive rate, consider using a mortgage broker. Brokers can negotiate deals for you with multiple lenders. Some brokers do take a commission from lenders. Before signing up for any broker, it is important to verify the fees.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

External Links

How To

How to find houses to rent

Finding houses to rent is one of the most common tasks for people who want to move into new places. Finding the perfect house can take time. When you are looking for a home, many factors will affect your decision-making process. These factors include price, location, size, number, amenities, and so forth.

We recommend you begin looking for properties as soon as possible to ensure you get the best deal. Ask your family and friends for recommendations. This way, you'll have plenty of options to choose from.